Weekly Economic Update – February 11, 2019

THE WEEK ON WALL STREET

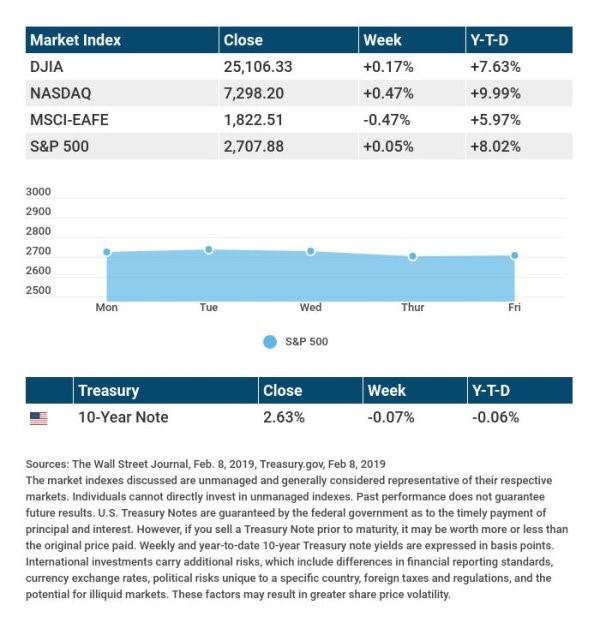

Major U.S. stock benchmarks eked out slight gains last week, with corporate profit reports and news about U.S.-China trade negotiations vying for investor attention over five trading sessions.

The big three ended the week little changed from where they settled the previous Friday. The Dow Jones Industrials rose 0.17%, while the S&P 500 Index gained 0.05%. The NASDAQ Composite ended the week up 0.47%. Looking at international stocks, the MSCI EAFE index retreated 0.47%. 1,2

eARNINGS SCORECARD

As of last Friday, 66% of all S&P 500 companies had reported fourth-quarter earnings. So far, 71% of these firms have announced earnings exceeding estimates, and 62% have seen revenues top projections. 3

Halfway through earnings season, 2019 future guidance has been a mixed bag for S&P 500 companies. For Wall Street, future earnings can be just as important as current earnings. We keep a close eye on both. 3

tariff TENSIONS

March 1 is the 90-day deadline set by President Trump for a trade deal with China. If no agreement is reached, the U.S. may consider a new round of tariffs. On Thursday, news that President Trump and Chinese President Xi may not meet before the March 1 deadline added to the market volatility.

The decision by the U.S. on new tariffs may hinge on how much progress has been made toward a new agreement. We do not expect that to become clear until the deadline nears.

STate of THE SERVICE SECTOR

Many indicators help economists take the pulse of the overall economy. The Institute for Supply Management keeps a critical, but not widely followed, index, which helps gauge the health of the service sector.

The January reading on this index came in at 56.7. Any reading above 50 shows that the service industry is seeing solid growth. 4

FINAL THOUGHT

Over the next several weeks, we are expecting more volatility as the markets digest economic news, a new wave of corporate earnings, and twists and turns on the geopolitical front. We will be watching to see if anything changes our short-term and long-term view. If you have any questions, do not hesitate to contact us.

T I P O F T H E W E E K

New parents should seek to create an emergency fund equivalent to 3-6 months of living expenses. Sticking to a budget can help a household save over time.

THE WEEK AHEAD: KEY ECONOMIC DATA

Wednesday: January’s Consumer Price Index, which measures monthly and yearly inflation.

Thursday: December retail sales figures (a delayed release due to the government shutdown).

Friday: January’s preliminary University of Michigan consumer sentiment index, a gauge of consumer confidence levels.

Source: Econoday / MarketWatch Calendar, February 8, 2019

The content is developed from sources believed to be providing accurate information. The forecasts or forward-looking statements are based on assumptions and may not materialize. The forecasts also are subject to revision. The release of data may be delayed without notice for a variety of reasons, including the shutdown of the government agency or change at the private institution that handles the material.

THE WEEK AHEAD: COMPANIES REPORTING EARNINGS

Monday: Loews Corp (L)

Tuesday: Activision Blizzard (ATVI), HubSpot (HUBS), Occidental Petroleum (OXY)

Wednesday: Cisco (CSCO), Hilton Worldwide Holdings (HLT), Yelp (YELP)

Thursday: Applied Materials (AMAT), CBS (CBS), Coca-Cola (KO)

Friday: Deere & Co. (DE), PepsiCo (PEP)

Source: Morningstar.com, February 8, 2019

Companies mentioned are for informational purposes only. It should not be considered a solicitation for the purchase or sale of the securities. Any investment should be consistent with your objectives, time frame and risk tolerance. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost. Companies may reschedule when they report earnings without notice.

Q U O T E O F T H E W E E K

“In all affairs it is a healthy thing now and then to hang a question mark on the things you have long taken for granted.”

BERTRAND RUSSELL

T H E W E E K L Y R I D D L E

I have no eyes, ears, tongue, or nose, yet I have the power to see, hear, taste, and smell everything . What am I?

LAST WEEK’S RIDDLE: You can throw a ball 25’ and make it come right back to you, without the ball hitting anything or being caught by anyone. How can you make this happen?

ANSWER: Throw the ball straight up in the air .

Tim Flick may be reached at 317-947-7047 or tflick@cornerfi.com www.cornerfi.com

Know someone who could use information like this?

Please feel free send us their contact information via phone or email. (Don’t worry – we’ll request their permission before adding them to our mailing list.)

Investment Advisor Representative, Cambridge Investment Research Advisors, Inc., a Registered Investment Advisor. Registered Representative, Securities offered through Cambridge Investment Research, Inc., a Broker/Dealer, Member FINRA/SIPC. Cambridge and Cornerstone Financial Advisory are not affiliated. This message distributed via use of the MarketingPro system.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. The information herein has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. Investments will fluctuate and when redeemed may be worth more or less than when originally invested. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All market indices discussed are unmanaged and are not illustrative of any particular investment. Indices do not incur management fees, costs and expenses, and cannot be invested into directly. All economic and performance data is historical and not indicative of future results. The Dow Jones Industrial Average is a price-weighted index of 30 actively traded blue-chip stocks. The NASDAQ Composite Index is a market-weighted index of all over-the-counter common stocks traded on the National Association of Securities Dealers Automated Quotation System. The Standard & Poor’s 500 (S&P 500) is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy. NYSE Group, Inc. (NYSE:NYX) operates two securities exchanges: the New York Stock Exchange (the “NYSE”) and NYSE Arca (formerly known as the Archipelago Exchange, or ArcaEx®, and the Pacific Exchange). NYSE Group is a leading provider of securities listing, trading and market data products and services. The New York Mercantile Exchange, Inc. (NYMEX) is the world’s largest physical commodity futures exchange and the preeminent trading forum for energy and precious metals, with trading conducted through two divisions – the NYMEX Division, home to the energy, platinum, and palladium markets, and the COMEX Division, on which all other metals trade. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. MarketingPro, Inc. is not affiliated with any person or firm that may be providing this information to you. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional.

CITATIONS:

1 – markets.wsj.com [2/8/19]

2 – quotes.wsj.com/index/XX/990300/historical-prices [2/8/19]

3 – insight.factset.com/earnings-season-update-february-8-2019 [2/8/19]

4 – instituteforsupplymanagement.org/ISMReport/NonMfgROB.cfm?SSO=1 [2/5/19]